In this article, you’ll learn about What is Economics? Definition, Meaning, Assumptions, Scope, Nature and more.

What is Economics

Economics is a social science that studies how individuals, businesses, and societies allocate scarce resources to satisfy unlimited wants and needs.

Meaning of Economics

At its core, economics explores how choices are made in the face of limited resources. It examines how individuals, businesses, and governments make decisions about production, consumption, and distribution of goods and services.

Economics Definition

Over time, the definition of economics has evolved:

Wealth Definition of Economics: Early economists, like Adam Smith, viewed economics primarily as the science of wealth creation. They focused on how to increase a nation’s wealth through trade, production, and accumulation of resources.

Welfare Definition of Economics: Later, the focus shifted to human welfare. Economists like Alfred Marshall emphasized the role of economics in improving the well-being of individuals and society.

Scarcity Definition of Economics: Lionel Robbins provided a more contemporary definition, emphasizing the central role of scarcity in economic decision-making. He defined economics as “the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses.”

Growth Definition of Economics: In modern times, economic growth has become a major focus, with economists studying how to increase the overall production and living standards of a nation.

Scope of Economics

Economics encompasses a wide range of topics, including:

Microeconomics: Focuses on individual economic units, such as consumers, producers, and markets.

Macroeconomics: Examines the overall performance of the economy, including national income, inflation, unemployment, and economic growth.

International Economics: Deals with economic interactions between countries, such as international trade, foreign exchange rates, and balance of payments.

Development Economics: Studies economic growth and development in developing countries.

Environmental Economics: Examines the economic impact of environmental issues and explores ways to promote sustainable economic development.

Financial Economics: Analyzes financial markets, including stocks, bonds, and other financial instruments.

5 Nature of Economics

Social Science: Economics is a social science because it deals with human behavior and social interactions.

Science of Choice: It focuses on how individuals and societies make choices in the face of scarcity.

Both Art and Science: Economics involves both the scientific method of analysis and the art of applying economic principles to real-world situations.

Assumptions in Economics

Economists often make simplifying assumptions to make their models more manageable:

Consumers have rational preferences: Consumers are assumed to make choices that maximize their own utility or satisfaction.

Existence of perfect competition: In many models, economists assume perfect competition, where there are many buyers and sellers, and no single buyer or seller can influence market prices.

Existence of equilibrium: Economists often analyze economic situations in terms of equilibrium, where supply and demand are balanced.

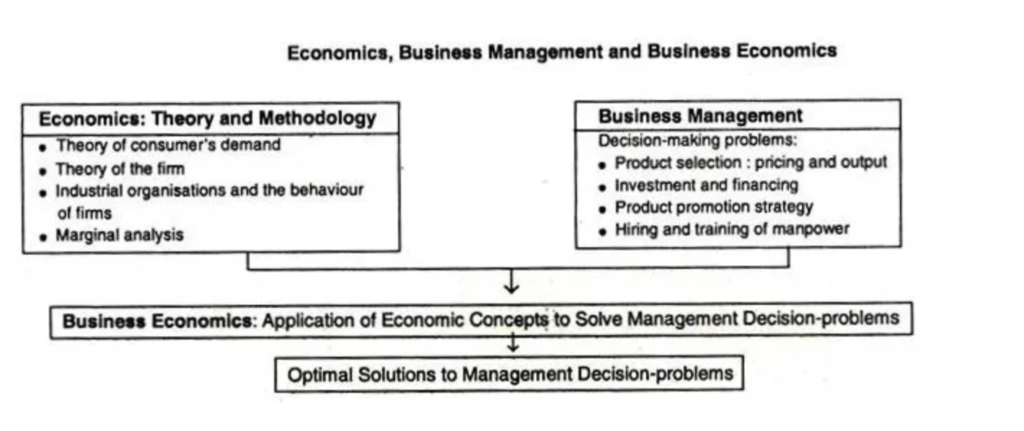

Difference Between Economics and Business Economics

Economics: A broader discipline that studies the overall economy and how it functions.

Business Economics: A specialized branch of economics that applies economic principles to business decision-making.

Business economics focuses on:

Pricing and output decisions

Market analysis and forecasting

Resource allocation within a firm

Investment and financial decisions

Conclusion

Economics is a multifaceted field that provides valuable insights into how individuals, businesses, and societies make decisions about resource allocation. By understanding economic principles, we can better understand the complexities of the world around us and make informed choices about economic policies and personal financial decisions.

In this article, you’ll learn about Basic Concepts of Economics and more.

Economics, often referred to as the “science of choice,” is a discipline that studies how individuals, businesses, and governments allocate scarce resources to satisfy unlimited wants and needs. It’s a complex field with many subfields, but understanding some fundamental concepts is essential for navigating the economic landscape.

Key Economic Concepts

Scarcity

Definition: The limited availability of resources compared to unlimited wants and needs.

Example: You only have ₹20 but want to buy a new video game (₹60), a pizza (₹15), and a movie ticket (₹10). You can’t afford all three, so you must choose one.

Opportunity Cost

Definition: The value of the next best alternative forgone.

Example: If you choose to spend your evening watching a movie, the opportunity cost is the time you could have spent studying or exercising.

Supply and Demand

Definition: The interaction between the quantity of a good or service that producers are willing to supply and the quantity that consumers are willing to demand at various prices.

Example: If the demand for a popular video game increases, the price will likely rise as well, as producers can charge more for the limited supply.

Want

Definition: A desire or wish for something.

Example: You want a new smartphone, a car, or a vacation.

Scale of Preference

Definition: A ranking of wants in order of their importance.

Example: If you have limited resources, you might prioritize your wants like this:

Food

Shelter

Clothing

Entertainment

Essentially, a scale of preference helps individuals make choices based on their limited resources. It’s a tool for allocating scarce resources to satisfy the most pressing wants.

Economic Systems

Definition: The system a country uses to organize and distribute goods and services.

Examples:

Market Economy: The United States, where individuals and businesses make most economic decisions.

Command Economy: North Korea, where the government controls most economic activity.

Mixed Economy: Most countries, like Canada and France, which combine elements of both market and command economies.

Economic Indicators

Definition: Measures used to assess the health of an economy.

Examples:

GDP (Gross Domestic Product): The total value of goods and services produced in a country.

Inflation: A general increase in prices over time.

Unemployment Rate: The percentage of the labor force that is unemployed.

Interest Rate: The cost of borrowing money.

Economic Growth

Definition: An increase in a nation’s production of goods and services over time.

Example: If a country’s GDP increases from one year to the next, it is experiencing economic growth.

Economic Cycles

Definition: Fluctuations in economic activity, characterized by periods of expansion and contraction.

Example: The business cycle, which includes periods of economic boom, recession, depression, and recovery.

Managerial Economics is both conceptual and metrical. Before the substantive decision problems which fall within the purview of managerial economics are discussed, it is useful to identify and understand some of the basic concepts underlying the subject.

Economic theory provides a number of concepts and analytical tools which can be of considerable and immense help to a manager in taking many decisions and business planning. This is not to say that economics has all the solutions. In fact, actual problem solving in business has found that there exists a wide disparity between economic theory of the firm and actual observed practice.

Therefore, it would be useful to examine the basic tools of managerial economics and the nature and extent of gap between the economic theory of the firm and the managerial theory of the firm. The contribution of economics to managerial economics lies in certain principles which are basic to managerial economics. There are six basic principles of managerial economics. They are:-

1. The Incremental Principle

The incremental concept is probably the most important concept in economics and is certainly the most frequently used in Managerial Economics. Incremental concept is closely related to the marginal cost and marginal revenues of economic theory.

The two major concepts in this analysis are incremental cost and incremental revenue. Incremental cost denotes change in total cost, whereas incremental revenue means change in total revenue resulting from a decision of the firm.

The incremental principle may be stated as follows:

A decision is clearly a profitable one if

(i) It increases revenue more than costs.

ii) It decreases some cost to a greater extent than it increases others.

(iii) It increases some revenues more than it decreases others.

(iv) It reduces costs more than revenues.

2. Marginal Principle

Marginal analysis implies judging the impact of a unit change in one variable on the other. Marginal generally refers to small changes. Marginal revenue is change in total revenue per unit change in output sold. Marginal cost refers to change in total costs per unit change in output produced (While incremental cost refers to change in total costs due to change in total output). The decision of a firm to change the price would depend upon the resulting impact/change in marginal revenue and marginal cost. If the marginal revenue is greater than the marginal cost, then the firm should bring about the change in price.

3. The Opportunity Cost Principle

Both micro and macro economics make abundant use of the fundamental concept of opportunity cost. In everyday life, we apply the notion of opportunity cost even if we are unable to articulate its significance. In Managerial Economics, the opportunity cost concept is useful in decision involving a choice between different alternative courses of action.

Resources are scarce, we cannot produce all the commodities. For the production of one commodity, we have to forego the production of another commodity. We cannot have everything we want. We are, therefore, forced to make a choice.

Opportunity cost of a decision is the sacrifice of alternatives required by that decision. Sacrifice of alternatives is involved when carrying out a decision requires using a resource that is limited in supply with the firm. Opportunity cost, therefore, represents the benefits or revenue forgone by pursuing one course of action rather than another.

The concept of opportunity cost implies three things:

(i) The calculation of opportunity cost involves the measurement of sacrifices.

(i1) Sacrifices may be monetary or real.

(iii) The opportunity cost is termed as the cost of sacrificed alternatives.

Opportunity cost is just a notional idea which does not appear in the books of account of the company. If resource has no alternative use, then its opportunity cost is nil.

In managerial decision making, the concept of opportunity cost occupies an important place. The economic significance of opportunity cost is as follows:

(i) It helps in determining relative prices of different goods.

(ii) It helps in determining normal remuneration to a factor of production.

(iii) It helps in proper allocation of factor resources.

4. Discounting Principle

This concept is an extension of the concept of time perspective. Since future is unknown and incalculable, there is lot of risk and uncertainty in future. Everyone knows that a rupee today is worth more than a rupee will be two years from now. This appears similar to the saying that “a bird in hand is more worth than two in the bush.” This judgment is made not on account of the uncertainty surrounding the future or the risk of inflation.

It is simply that in the intervening period a sum of money can earn a return which is ruled out if the same sum is available only at the end of the period. In technical parlance, it is said that the present value of one rupee available at the end of two years is the present value of one rupee available today. The mathematical technique for adjusting for the time value of money and computing present value is called ‘discounting’.

5. Concept of Time Perspective Principle

The time perspective concept states that the decision maker must give due consideration both to the short run and long run effects of his decisions. He must give due emphasis to the various time periods. It was Marshall who introduced time element in economic theory.

The economic concepts of the long run and the short run have become part of everyday language. Managerial economists are also concerned with the short run and long run effects of decisions on revenues as well as costs. The main problem in decision making is to establish the right balance between long run and short run.

In the short period, the firm can change its output without changing its size. In the long period, the firm can change its output by changing its size. In the short period, the output of the industry is fixed because the firms cannot change their size of operation and they can vary only variable factors. In the long period, the output of the industry is likely to be more because the firms have enough time to increase their sizes and also use both variable and fixed factors.

In the short period, the average cost of a firm may be either more or less than its average revenue. In the long period, the average cost of the firm will be equal to its average revenue. A decision may be made on the basis of short run considerations, but may as time elapses have long run repercussions which make it more or less profitable than it at first appeared.

6. Equi-Marginal Principle

One of the widest known principles of economics is the equi-marginal principle. The principle states that an input should be allocated so that value added by the last unit is the same in all cases. This generalization is popularly called the equi-marginal.

Let us assume a case in which the firm has 100 unit of labour at its disposal. And the firm is involved in five activities viz., A, B, C, D and E. The firm can increase any one of these activities by employing more labour but only at the cost i.e., sacrifice of other activities.

An optimum allocation cannot be achieved if the value of the marginal product is greater in one activity than in another. It would be, therefore, profitable to shift labour from low marginal value activity to high marginal value activity, thus increasing the total value of all products taken together.

Many new subjects have evolved in recent years due to the interaction among basic disciplines. While there are many such new subjects in natural and social sciences, managerial economics can be taken as the best example of such a phenomenon among social sciences. Hence it is necessary to trace its roots and relationship with other disciplines.

1. Relationship with economics

The relationship between managerial economics and economics theory may be viewed form the point of view of the two approaches to the subject Viz. Microeconomics and Marco Economics. Microeconomics is the study of the economic behaviour of individuals, firms and other such micro-organization. Managerial economics is rooted in Micro Economic theory. Managerial Economics makes use to several Micro Economic concepts such as marginal cost, marginal revenue, elasticity of demand as well as price theory and theories of market structure to name only a few. Macro theory on the other hand is the study of the economy as a whole. It deals with the analysis of national income, the level of employment, general price level, consumption and investment in the economy and even matters related to international trade, Money, public finance, etc.

The relationship between managerial economics and economics theory is like that of engineering science to physics or of medicine to biology. Managerial economics has an applied bias and its wider scope lies in applying economic theory to solve real life problems of enterprises. Both managerial economics and economics deal with problems of scarcity and resource allocation.

2. Management theory and accounting

Managerial economics has been influenced by the developments in management theory and accounting techniques. Accounting refers to the recording of pecuniary transactions of the firm in certain books. A proper knowledge of accounting techniques is very essential for the success of the firm because profit maximization is the major objective of the firm.

Managerial Economics requires a proper knowledge of cost and revenue information and their classification. A student of managerial economics should be familiar with the generation, interpretation and use of accounting data. The focus of accounting within the firm is fast changing from the concepts of store keeping to that if managerial decision making, this has resulted in a new specialized area of study called “Managerial Accounting”.

3. Managerial Economics and mathematics

The use of mathematics is significant for managerial economics in view of its profit maximization goal long with optional use of resources. The major problem of the firm is how to minimize cost, how to maximize profit or how to optimize sales. Mathematical concepts and techniques are widely used in economic logic to solve these problems. Also mathematical methods help to estimate and predict the economic factors for decision making and forward planning.

Mathematical symbols are more convenient to handle and understand various concepts like incremental cost, elasticity of demand etc., Geometry, Algebra and calculus are the major branches of mathematics which are of use in managerial economics. The main concepts of mathematics like logarithms, and exponential, vectors and determinants, input-output models etc., are widely used. Besides these usual tools, more advanced techniques designed in the recent years viz. linear programming, inventory models and game theory fine wide application in managerial economics.

4. Managerial Economics and Statistics

Managerial Economics needs the tools of statistics in more than one way. A successful businessman must correctly estimate the demand for his product. He should be able to analyses the impact of variations in tastes.

Fashion and changes in income on demand only then he can adjust his output. Statistical methods provide and sure base for decision-making. Thus, statistical tools are used in collecting data and analyzing them to help in the decision making process.

Statistical tools like the theory of probability and forecasting techniques help the firm to predict the future course of events. Managerial Economics also make use of correlation and multiple regressions in related variables like price and demand to estimate the extent of dependence of one variable on the other. The theory of probability is very useful in problems involving uncertainty.

5. Managerial Economics and Operations Research

Taking effective decisions is the major concern of both managerial economics and operations research. The development of techniques and concepts such as linear programming, inventory models and game theory is due to the development of this new subject of operations research in the postwar years. Operations research is concerned with the complex problems arising out of the management of men, machines, materials and money.

Operation research provides a scientific model of the system and it helps managerial economists in the field of product development, material management, and inventory control, quality control, marketing and demand analysis. The varied tools of operations Research are helpful to managerial economists in decision-making.

6. Managerial Economics and the theory of Decision making

The Theory of decision-making is a new field of knowledge grown in the second half of this century. Most of the economic theories explain a single goal for the consumer i.e., Profit maximization for the firm. But the theory of decision-making is developed to explain multiplicity of goals and lot of uncertainty.

As such this new branch of knowledge is useful to business firms, which have to take quick decision in the case of multiple goals. Viewed this way the theory of decision making is more practical and application oriented than the economic theories.

7. Managerial Economics and Computer Science

Computers have changed the way of the world functions and economic or business activity is no exception.

Computers are used in data and accounts maintenance, inventory and stock controls and supply and demand predictions. What used to take days and months is done in a few minutes or hours by the computers. In fact computerization of business activities on a large scale has reduced the workload of managerial personnel. In most countries a basic knowledge of computer science, is a compulsory programme for managerial trainees.

To conclude, managerial economics, which is an offshoot traditional economics, has gained strength to be a separate branch of knowledge. It strength lies in its ability to integrate ideas from various specialized subjects to

gain a proper perspective for decision-making.

A successful managerial economist must be a mathematician, a statistician and an economist. He must be also able to combine philosophic methods with historical methods to get the right perspective only then; he will be good at predictions. In short managerial practices with the help of other allied sciences.

Business economics is a field of applied economics that studies the financial, organizational, market-related, and environmental issues faced by corporations. Economic theory and quantitative methods form the basis of assessments on factors affecting corporations such as business organization, management, expansion, and strategy. Studies might include how and why corporations expand, the impact of entrepreneurs, the interactions among corporations, and the role of governments in regulation.

The Basics of Business Economics

Economics, broadly, refers to the study of the components and functions of a particular marketplace or economy, such as supply and demand, and the effect of the concept of scarcity. Within an economy, production factors, distribution methods, and consumption are important subjects of study. Business economics focuses on the elements and factors within business operations and how they relate to the economy as a whole.

The field of business economics addresses economic principles, strategies, standard business practices, the acquisition of necessary capital, profit generation, the efficiency of production, and overall management strategy. Business economics also includes the study of external economic factors and their influence on business decisions such as a change in industry regulation or a sudden price shift in raw materials.

Real World Example of Business Economics

There are various organizations associated with the field of business economics. In the United States, the National Association for Business Economics (NABE) is the professional association for business economists. The organization’s mission is “to provide leadership in the use and understanding of economics.” In the United Kingdom, the equivalent organization is the Society of Business Economists.

Economic theory and quantitative methods form the basis of microeconomic assessments of factors

affecting corporations.

Business economics encompasses subjects such as the concept of scarcity, product factors, distribution, and consumption.

Managerial economics is one important offshoot of business economics.

The National Association for Business Economics (NABE) is the professional association for business economists in the United States.

Nature of Business Economics

(i) Business Economics is a Science

What is Science? It is simply a systematic body of knowledge which can establish a relationship between cause and effect.

Further, Mathematics, Statistics, and Econometrics are decision sciences.

Business Economics integrates these decision sciences with Economic Theory to arrive at strategies to help businesses achieve their goals. Hence, it follows scientific methods and also tests the validity of the results. This is one aspect of the nature of business economics.

(ii) It is based on Micro Economics

We understand the basic difference between micro and macroeconomics. A business manager is certainly more concerned about achieving the objectives of his own organization. After all, this helps him in ensuring profits and long-term survival of the firm.

Business Economics is more concerned with the decision-making situations of individual establishments. Therefore, it depends on the techniques of Microeconomics.

(iii) It Incorporates Elements of Macro Analysis

Even though all businesses focus on their profitability and survival, a firm cannot operate in a vacuum. The external environment of the economy like income and employment levels in the economy, tax policies, etc., affects the firm. All these external factors are components of macro economy.

Therefore, a business manager has to take all such factors into consideration which may influence his business environment.

(iv) It is an Art

Business Economics is an art as it requires the practical application of rules and principle to achieve set objectives.

(v) Use of Theory of Markets and Private Enterprises

Business Economics primarily uses the theory of markets and private enterprises. It uses the theory of the firm and resource allocation in a private enterprise economy.

(vi) Pragmatic in Approach

Microeconomics is purely theoretical and analyzes economic occurrences under unrealistic assumptions. On the other hand, Business Economics is pragmatic in its approach. It tries to solve the problems which the firms face in the real world.

(vii) Interdisciplinary

Business Economics incorporates tools from many other disciplines like mathematics, statistics, accounting, marketing, etc. Therefore, is in interdisciplinary in nature.

(viii) Normative

Broadly speaking, Economic Theory has evolved along two lines – Positive and Normative.

A positive or pure science analyzes the cause and effect relationship between variables in a scientific manner. However, it does not involve any value judgment. In simpler words, it describes the economic behavior of individuals or society without focusing on the desirability of such behavior.

On the other hand, normative science involves value judgments. It suggests a course of action under the given circumstances.

Usually, Business Economics is normative in nature. It offers suggestions for the application of economic principles while forming policies, making decisions, and planning for the future. However, firms must understand their environment thoroughly to establish decision rules. This requires the study of positive economic theory.

Therefore, we can say that Business Economics combines the essentials of both the theories while keeping more emphasis on the normative economic theory.

The Scope of Business Economics

1. Microeconomics Applied to Operational Issues

As the name suggests, internal or operational issues are issues that arise within a firm and are within the control of the management. It is within the scope of business economics to analyze this.

Further, a few examples of such issues are choice of business, size of business, product designs, pricing, promotion for sales, technology choice, etc. Most firms can deal with these using the following microeconomics theories:

(i) Analyzing Demand and Forecasting

Analyzing demand is all about understanding buyer behavior. It studies the preferences of consumers along with the effects of changes in the determinants of demand. Also, these determinants include the price of the good, consumer’s income, tastes/ preferences, etc.

Forecasting demand is a technique used to predict the future demand for a good and/or service. Further, this prediction is based on the past behavior of factors which affect the demand. This is important for firms as accurate predictions help them produce the required quantities of goods at the right time.

Further, it gives them enough time to arrange various factors of production in advance like raw materials, labor, equipment, etc. Business Economics offers scientific tools which assist in forecasting demand.

(ii) Production and Cost Analysis

A business economist has the following responsibilities with regards to the production:

Decide on the optimum size of output based on the objectives of the firm.

Also, ensure that the firm does not incur any undue costs.

By production analysis, the firm can choose the appropriate technology offering a technically efficient way of producing the output. Cost analysis, on the other hand, enables the firm to identify the behavior of costs when factors like output, time period, and the size of plant change. Further, by using both these analyses, a firm can maximize profits by producing optimum output at the least possible cost.

(iii) Inventory Management

Firms can use certain rules to reduce costs associated with maintaining inventory in the form of raw materials, work in progress, and finished goods. Further, it is important to understand that the inventory policies affect the profitability of a firm. Hence, economists use methods like the ABC analysis and mathematical models to help the firm in maintaining an optimum stock of inventories.

(iv) Market Structure and Pricing Policies

Any firm needs to know about the nature and extent of competition in the market. A thorough analysis of the market structure provides this information. Further, with the help of this, firms command a certain ability to determine prices in the market. Also, this information helps firms create strategies for market management under the given competitive conditions.

Price theory, on the other hand, helps the firm in understanding how prices are determined under different kinds of market conditions. Also, it assists the firm in creating pricing policies.

(v) Resource Allocation

Business Economics uses advanced tools like linear programming to create the best course of action for an optimal utilization of available resources.

(vi) Theory of Capital and Investment Decisions

Among other decisions, a firm must carefully evaluate its investment decisions an allocate its capital sensibly. Various theories pertaining to capital and investments offer scientific criteria for choosing investment projects. Further, these theories also help the firm in assessing the efficiency of capital. Business Economics assists the decision-making process when the firm needs to decide between competing uses of funds.

(vii) Profit Analysis

Profits depend on many factors like changing prices, market conditions, etc. The profit theories help firms in measuring and managing profits under such uncertain conditions. Further, they also help in planning future profits.

(viii) Risk and Uncertainty Analysis

Most businesses operate under a certain amount of risk and uncertainty. Also, analyzing these risks and uncertainties can help firms in making efficient decisions and formulating plans.

2. Macroeconomics applied to Environmental Issues

External or environmental factors have a measurable impact on the performance of a business. The major macroeconomic factors are:

Type of economic system

Stage of the business cycle

General trends in national income, employment, prices, saving, and investment.

Government’s economic policies

Performance of the financial sector and capital market

Socio-economic organizations

Social and political environment.

The management of a firm has no control over these factors. Therefore, it is important that the firm fine-tunes its policies to minimize the adverse effects of these factors.