For businesses to operate successfully, they need to be able to anticipate future trends and events. This is where forecasting comes in. Forecasting is the process of making predictions about the future based on past data and current trends. It is an essential tool for businesses of all sizes, as it allows them to make informed decisions about everything from production levels to marketing campaigns.

What is Forecasting

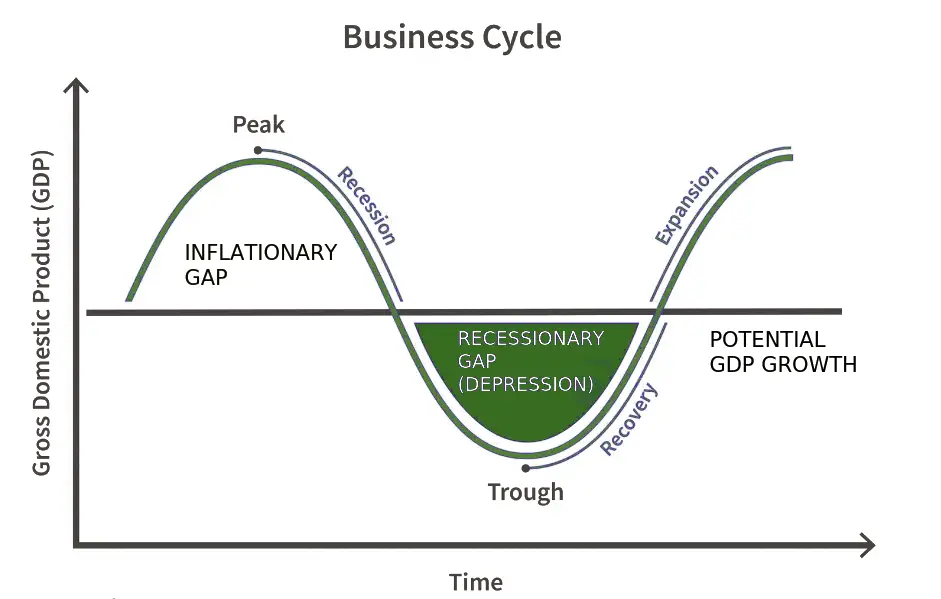

Forecasting involves predicting future events that can impact a business. By analyzing past data, identifying trends, and considering current conditions, businesses can anticipate future sales, finances, customer demand, and market shifts. This information empowers informed decision-making, effective planning, and proactive risk management. Forecasting methods encompass a range of techniques, from analyzing historical data to employing sophisticated statistical models. However, it’s crucial to acknowledge that the future is inherently uncertain. Unforeseen events can significantly impact the accuracy of forecasts, necessitating regular review and updates as new information becomes available.

Nature of Forecasting

Forecasting involves utilizing past data, identifying trends, and recognizing patterns to make informed predictions about future events or outcomes. This practice is fundamental for effective planning and decision-making across various fields, including business, finance, economics, and meteorology.

Key aspects of forecasting include:

- Goal-Oriented Focus: The primary objective of forecasting is to support informed decision-making, effective risk management, and strategic planning to achieve specific goals and objectives.

- Inherent Uncertainty: The future is inherently unpredictable. Unexpected events or factors can significantly impact the accuracy of any forecast.

- Reliance on Assumptions: Forecasting often relies on specific assumptions about future conditions. If these assumptions prove inaccurate, the forecast’s reliability diminishes.

- Time Horizon Variability: Forecasts can be generated for different timeframes, such as short-term, medium-term, and long-term. Generally, the accuracy of predictions decreases as the forecast horizon extends further into the future.

- Diverse Methodologies: A wide range of methods and techniques are employed in forecasting, encompassing both qualitative approaches (such as expert opinions and market research) and quantitative methods (such as statistical modeling and data analysis).

- Continuous Adaptation: Forecasting is an ongoing process that necessitates regular review and updates. New information, changes in market conditions, and shifts in underlying assumptions require adjustments to the forecast.

Planning and Forecasting

Planning and forecasting are interconnected processes crucial for effective decision-making and resource allocation.

- Planning: Involves setting goals, determining the best course of action to achieve those goals, and efficiently utilizing resources (time, money, and personnel).

- Forecasting: Involves making educated predictions about future events or trends based on past data, patterns, and statistical analysis.

Forecasting provides the essential information and predictions that guide the planning process. Conversely, planning helps organizations determine priorities and allocate resources based on the forecasted outcomes. For example, a business can use sales forecasts to determine production levels, marketing strategies, and staffing needs. This allows the company to create a detailed plan to achieve its sales targets and effectively utilize its resources.

Importance of Forecasting in Business

Forecasting plays a vital role in business success by:

- Improving Decision-Making: By anticipating future events, businesses can make more informed decisions, increasing their chances of success.

- Optimizing Resource Allocation: Forecasting helps businesses allocate resources effectively, such as adjusting production levels, staffing requirements, and budgets to meet anticipated demand.

- Mitigating Risks: By identifying potential risks and uncertainties, businesses can develop contingency plans and strategies to minimize potential negative impacts.

- Setting Realistic Goals: Forecasting enables businesses to set achievable goals and targets, providing a framework for monitoring progress and making necessary adjustments.

- Improving Financial Planning: Accurate financial forecasts are crucial for budgeting and financial planning, enabling businesses to estimate revenues, costs, and cash flow effectively.

- Optimizing Supply Chain Management: Forecasting helps optimize inventory levels, reduce stockouts, and minimize holding costs by predicting demand and ensuring a smooth flow of goods within the supply chain.

Limitations of Forecasting

Despite its importance, forecasting has inherent limitations:

- Uncertainty: The future is inherently uncertain, and unforeseen events can significantly impact the accuracy of any forecast.

- Data Dependence: The accuracy of forecasts relies heavily on the quality and completeness of the data used. Inaccurate or incomplete data can lead to unreliable predictions.

- Assumption Reliance: Forecasts often rely on assumptions about future conditions, which may not always hold true.

- Complexity: Forecasting can be a complex process, especially when dealing with large datasets and sophisticated models.

- Time-Consuming: The process of developing and maintaining accurate forecasts can be time-consuming, requiring ongoing data collection, analysis, and updates.

- Limited Scope: Forecasts may not always account for all possible factors or unforeseen events, potentially limiting their accuracy and applicability.